Navigating the world of online loans can be tricky, especially when it comes to understanding interest rates. That’s where interest rate calculators come into play. These handy tools can help you figure out how much you’ll pay over time, making it easier to choose the right loan for your needs.

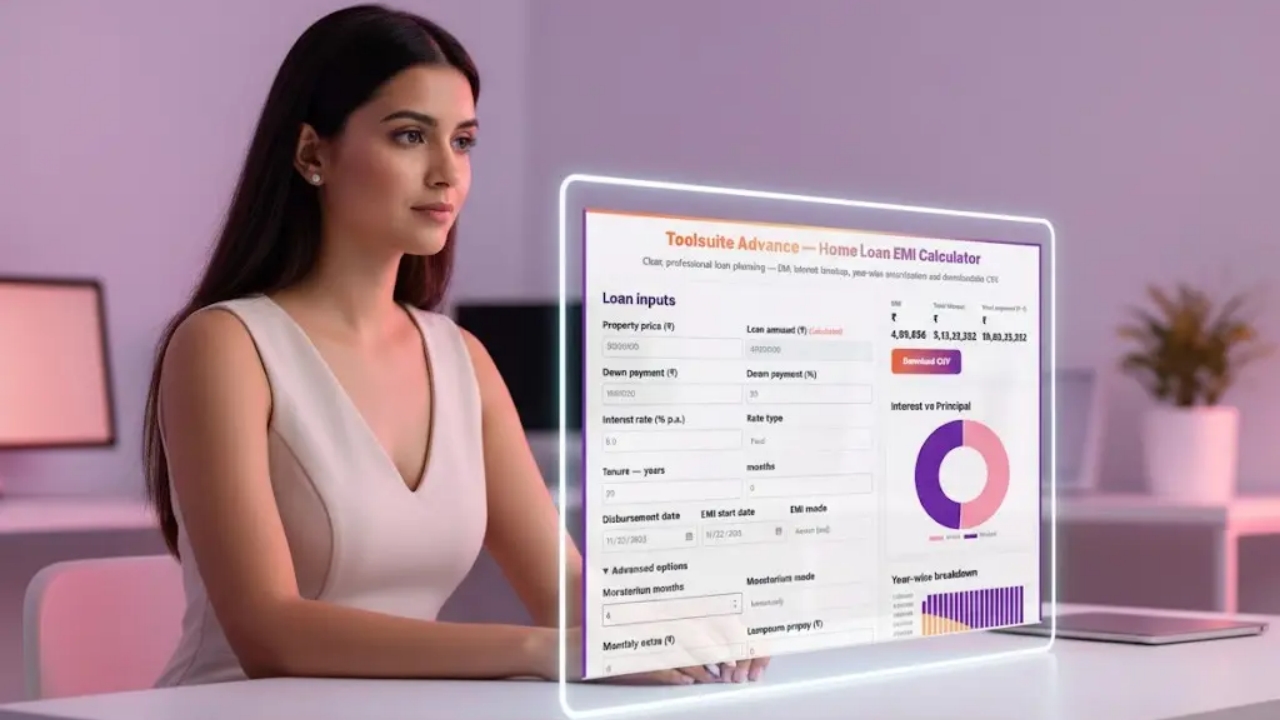

Finding a reliable interest rate calculator is essential. Many financial websites and lending platforms offer these tools for free, so you have plenty of options. Look for a calculator that allows you to input key loan parameters like the amount you want to borrow, the interest rate, and the loan term. A good calculator will give you a clear breakdown of your monthly payments and the total interest you’ll pay over the life of the loan.

Once you have the calculator ready, start by entering the loan amount. This is the principal, or the total amount you’re looking to borrow. Next, input the interest rate. If you’re unsure about what rate you might qualify for, do a bit of research on average rates based on your credit score. This is a crucial step because even a small difference in the interest rate can lead to significant changes in your total repayment amount.

After you’ve entered the loan amount and interest rate, you’ll need to specify the loan term. This is usually expressed in months or years. A longer loan term often means lower monthly payments, but keep in mind that you’ll end up paying more in interest over time. Conversely, a shorter loan term may lead to higher monthly payments but less interest paid overall. Use the calculator to play around with different terms and see how they affect your payments.

Once you’ve filled in all the necessary information, click the calculate button. The results will show you your estimated monthly payment, total interest paid, and total repayment amount. Take a moment to analyze these figures. If the monthly payment looks too high for your budget, consider adjusting either the loan amount or the term. This is a great way to visualize how different factors influence your loan.

Another useful approach is to compare multiple loan offers using the calculator. If you’re looking at loans from different lenders, input the same loan amount and term for each one. This side-by-side comparison can help you identify which lender offers the best deal. Remember, the lowest monthly payment isn’t always the best option if it comes with a higher interest rate.

Some calculators allow you to factor in additional costs like fees or insurance. If your loan includes these extras, make sure to include them in your calculations to get a clearer picture of your total costs.

Don’t hesitate to reach out to lenders if you have questions about their rates or terms. Understanding the details can help you avoid surprises later on. Interest rate calculators are a great starting point, but having a conversation with your lender can provide clarity on any specific concerns you might have.

Using interest rate calculators effectively can make a significant difference in your borrowing experience. By taking the time to understand how these tools work, you can make more informed choices that align with your financial goals.